What is VSLA anyway?

Here on the Thai/Burma border, refugee families do not have access to reliable financial services. All they have is cash under the pillow and willpower. When you are working in the hot sun for 9 hours your willpower runs out and then your money runs out. When the money runs out you have nothing for education, investment, or emergencies. The only place to turn is black-market lenders lending at 20%/month…and you end up in a vicious debt cycle.

We provide a solution to these families. We provide legitimate and secure financial infrastructure that empowers. We use the VSLA model.

Care International developed the Village Savings and Loan Association model more than 30 years ago in Africa. Since then, people have used the VSLA to bring financial growth and resilience to families and communities all over the world.

It is easy to confuse VSLA with Micro Finance. Especially normal people who are not technical specialists in the aid and development field. So don’t feel bad if you are thinking of Micro Finance. Be excited that you get to learn something really cool.

The Micro Finance is an organization or company making small loans to very poor people (the kind of loans and clients that a traditional bank doesn’t’ want to work with.)

In the VSLA model, an organization trains a community to form their own micro savings and loan (think of the movie “It’s A Wonderful Life”) or credit union. Many of us have accounts at credit unions. When you open an account at a credit union you apply to become a member. As a member you deposit money, borrow money, and gain access to whatever other member benefits that credit union provides.

Just like a bank, in a credit union you get money added to your deposits. With a bank you are getting interest at an interest rate connected to the rate set by the Federal Reserve. However, with a credit union the money added to your savings is a share in the revenue generated by the credit union investing your deposits in loans to members, in market investments, etc. You don’t receive interest; you are receiving dividends from the investment of your deposits.

Now, imagine the credit union or savings and loan on a micro scale and you get a good idea of what a VSLA is.

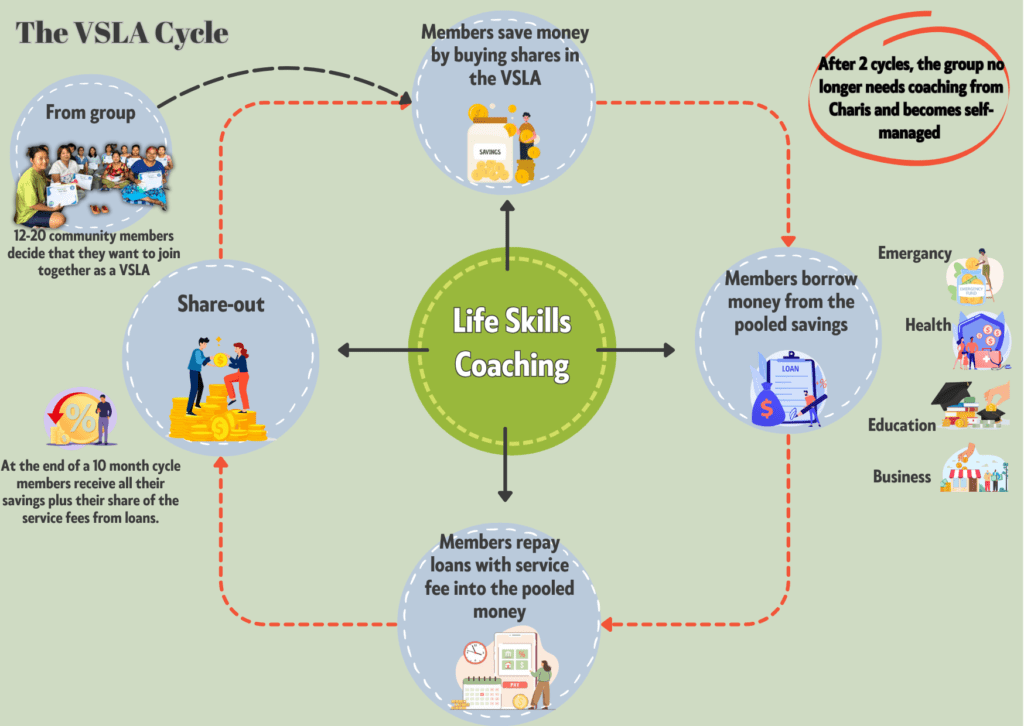

A community, whether it is a group of bamboo huts or an apartment block, decides to start a VSLA. The people in the community who want to join become members. They save their money together in the form of buying shares in the group. They borrow from that pooled savings. They pay reasonable service fees on that loan. Those service fees become the dividends distributed to all the members according to how many shares they own.

Charis VSLA’s run in cycles of 10 months. At the end of a cycle all the savings and dividends get shared out to the members then they start a new cycle.

During the cycle, members borrow mainly for emergencies, school fees and expenses, investments in their micro-businesses, etc. The other members vote on the loans…this means that your neighbors are your credit score.

The group carries out all the processes of saving and lending transparently, in front of all the members. This gives security. Even more than that, it creates a community of accountability. It builds mutual trust. That trust spreads out into the rest of the life of the community. Once dark and fragmented villages become communities of trusting and collaborative problem solvers.

When children live in this transformed situation, they learn the financial responsibility and ownership their parents are practicing. Also, they grow up in a brighter, more collaborative community. Add these things to the greater financial resilience of their family and you get a generation with greater opportunity that thinks differently. You break the cycle of generational poverty.

Aaron is the co-founder of The Charis Project. He is the current CEO also. In Thailand he is president and director of Shade Tree Foundation, our Thai partner foundation.